Climate Finance Approach for Railway Projects in Africa

Frédéric Mao, Senior Policy Advisor supporting the African Union Program for the Development of Infrastructure in Africa (PIDA), provided an insightful overview of climate finance options for railway projects at the African Union Commission (AUC)’s Department of Infrastructure and Energy (IED) Continental Workshop. The workshop, focused on the implementation of the Africa Integrated Railways Network (AIRN), took place from 7th to 10th May 2024 in Dar es Salaam, Tanzania.

Climate Finance for Railway Projects

Railway projects, like any infrastructure project, undergo a “lifecycle” that includes project preparation funding, project financing, and operations and maintenance. GIZ’s Green Infrastructure Corridors for Intra-African Trade project has prioritised assisting the African Union (AUC and AUDA-NEPAD) in planning for low-carbon and climate-resilient infrastructure projects and mobilising climate finance for PIDA projects.

Climate change adaptation involves actions to reduce vulnerability to climate impact, while climate mitigation focuses on reducing or preventing greenhouse gas emissions. Mao pointed out the significant investment needed for railway projects, citing a McKinsey Institute estimate of an additional US$300 billion annually to keep pace with economic growth and achieve climate resilience. In low and middle-income countries, the investment needs in the railway industry range from US$25 to US$80 billion per year between now and 2050.

Despite the substantial need, railway projects face significant challenges in attracting climate finance. Dedicated funds like the Green Climate Fund (GCF) are not scaled to handle the massive capital expenditures required for these projects. Mao noted that the only GCF investment in railways is a light train project in Costa Rica, underscoring the gap in funding for larger projects. Generally speaking, there is limited investment in road and transport projects through climate finance. The reason for this gap is that climate funds are not designed to address the sheer amount of funding needed for large-scale railway projects. These projects require substantial capital expenditure, which dedicated climate funds are not adequately scaled to support.

One of the challenges with railway projects is that their primary source of funding is government revenue. Additionally, there are issues related to harmonisation, such as transitioning from Cape gauge or Meter gauge to the Standard Gauge Railway.

Investment risk is a major barrier in low and middle-income countries, where issues such as macroeconomic instability, currency volatility, and political instability deter investors. Mao emphasised the importance of domestic resource mobilisation strategies, suggesting that local resources could be a viable alternative to traditional concessional aids and multilateral development banks. He highlighted that it is a mindset issue when it comes to financing this type of infrastructure. Typically, the first move is to think about concessional aids or multilateral development banks. However, the necessary funds are often available locally. Mao stressed the importance of being able to mobilise effective funding that meets the needs of the project, rather than focusing solely on traditional climate finance sources.

Leveraging Climate Finance

What is interesting is that private sector climate finance resources could potentially meet the entire rail financing gap, something that none of the dedicated Climate Finance Funds can do on a standalone basis.

Carbon market finance is a promising avenue to explore, particularly for financing or refinancing eligible projects linked to electrified and low-carbon rail infrastructure for passenger and freight transport. It comes down to how we leverage these instruments collectively, with climate funds serving as potential co-financiers for railway projects.

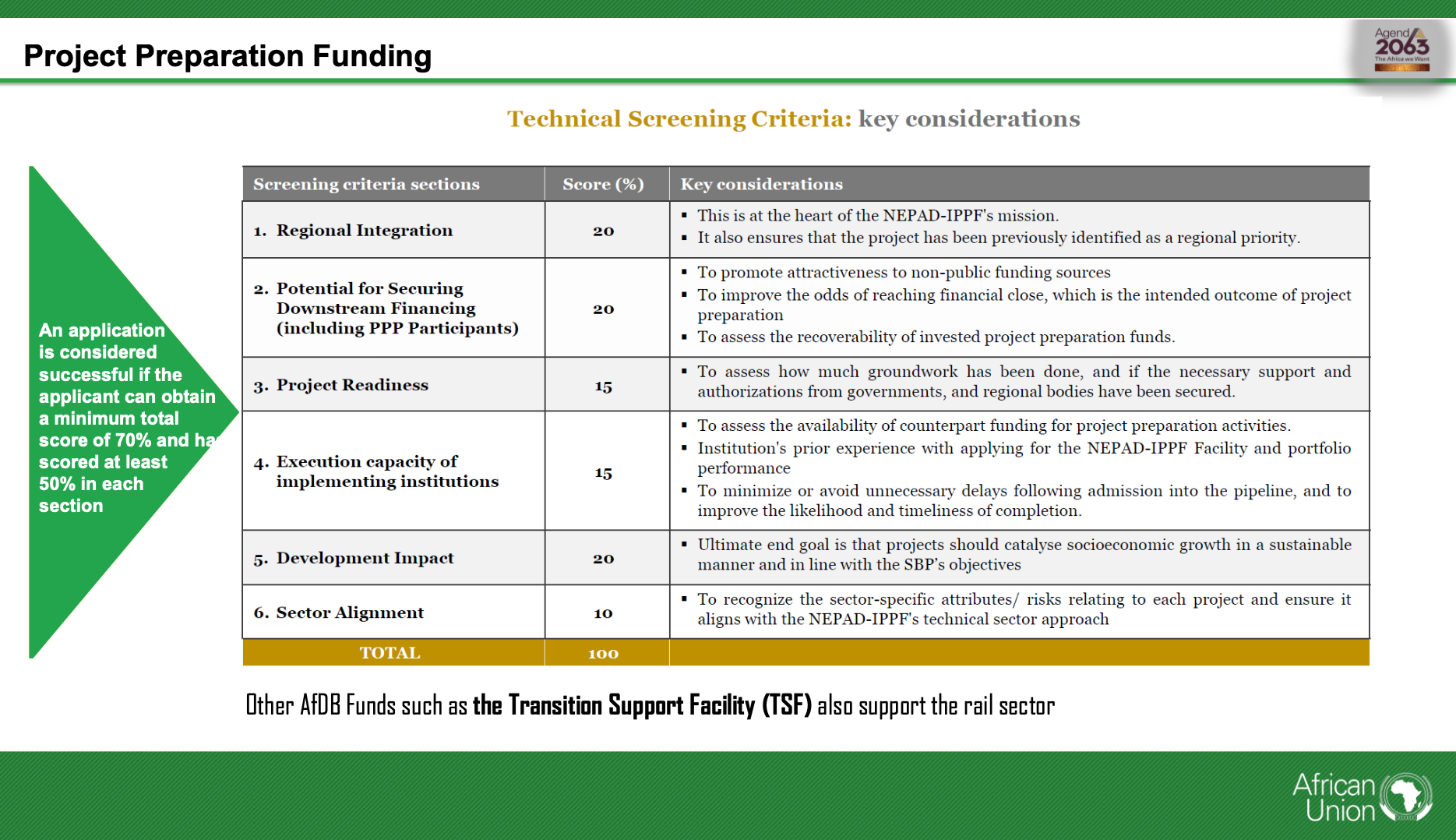

Effective project preparation funding is crucial. Mao highlighted the NEPAD Infrastructure Project Preparation Facility (IPPF), which has funded feasibility studies for railway projects since 2014. GIZ has also funded the Special Delivery Mechanism (SDM) to facilitate project entry into the NEPAD IPPF. However, awareness and access to these tools remain limited.

The NEPAD IPPF can provide grants ranging from US$700,000 to US$2 million.

Mao shared a successful case study from Côte d’Ivoire—the Abidjan light train (Métro d’Abidjan). Initially, the project faced challenges in securing €30 million for preliminary work due to the need for sovereign guarantees, among other requirements. Eventually, a private commercial bank provided the loan without such guarantees, demonstrating the potential of leveraging local resources for project funding.

“We looked at the concession agreement and found that there was a termination indemnity and severance indemnity that we could pledge and assign to the lenders,” Mao explained. There were two exit mechanisms: either the project gets refinanced by long-term lenders like a multilateral development bank, or if the project is unable to secure long-term financing, the termination fee would be used to repay the outstanding loans.

As of now, the project has been funded by the Agence Française de Développement to the tune of US$1.9 billion. At that time, the borrower repaid the initial loan from the private bank. “What I’m trying to stress here,” Mao continued, “is that there was no need to search globally for funding. The money was available locally. One private commercial bank provided the €30 million loan without requiring any sovereign guarantees or complicated arrangements.”

This case demonstrates the potential of local resources and innovative financial structuring in overcoming funding challenges for infrastructure projects. This process can also be duplicated for other projects.

Projects like the light train transit for the greater metropolitan area in Costa Rica, financed by the Green Climate Fund (GCF), illustrate how seed money can attract additional funding. The project, approved in 2021, had a total financing of US$1.9 billion, with the GCF contributing approximately US$300 million. The remaining funds were secured from other financiers.

What is particularly interesting about this project is the co-financing ratio, which was around 15 to 85. This means that the seed money from the GCF enabled the project sponsor to leverage and secure more than eight times the amount invested by the GCF. This example highlights the potential of leveraging climate finance to achieve long-term project goals.

The Costa Rican light train project demonstrates how seed money can be effectively used to attract substantial long-term financing. The same principle applies to the Métro d’Abidjan project in Côte d’Ivoire. In that case, a bridging loan was provided by a private commercial bank, which was later refinanced by long-term lenders.

In terms of prioritisation of climate finance facilities, the Green Climate Fund stands out as a significant contributor. At least one successful experience with the light train in Costa Rica demonstrates the fund’s potential to support large infrastructure projects.

Another example provided was the inaugural Bond issued in 2022 for US$95 million. A local currency Green Bond issued by the ONCF – Morocco Railways, with the support of the World Bank. ONCF was the first company in Africa to issue a corporate Green Bond for sustainable mobility projects. The World Bank supported the Government of Morocco and the railway to structure compensation for public services and restructure ONCF’s balance sheet, shedding certain debt. The technical assistance offered played a crucial role in readying ONCF to be creditworthy.

A mix of climate finance, carbon credits and green bonds could deliver the finance required to execute railway projects. Unlocking these potential sources of financing will pave the way for the decarbonisation of transport and lasting sustainable economic development for Africa.

The African Union Commission has an initiative underway to establish a carbon credit market in Africa under the Sustainable Environment and Blue Economy Directorate. This directorate is organising a continental carbon market conference, aiming to create a robust carbon market that includes railways as a key candidate for carbon finance.